July 29, 2024

DroneShield: Australia’s Only Anti-Drone Tech Company

For investors who keep track of the markets, there is no better description for DroneShield (DRO.AU) than being this year’s ASX dark horse. Once a relatively unknown small cap, DroneShield has emerged to become Superhero’s most traded stock of 2024, beating the likes of Tesla, NVIDIA, Pilbara Minerals and Qantas. But perhaps that’s unsurprising – DroneShield’s…

By Stella Ong

Scan this article:

For investors who keep track of the markets, there is no better description for DroneShield (DRO.AU) than being this year’s ASX dark horse.

Once a relatively unknown small cap, DroneShield has emerged to become Superhero’s most traded stock of 2024, beating the likes of Tesla, NVIDIA, Pilbara Minerals and Qantas.

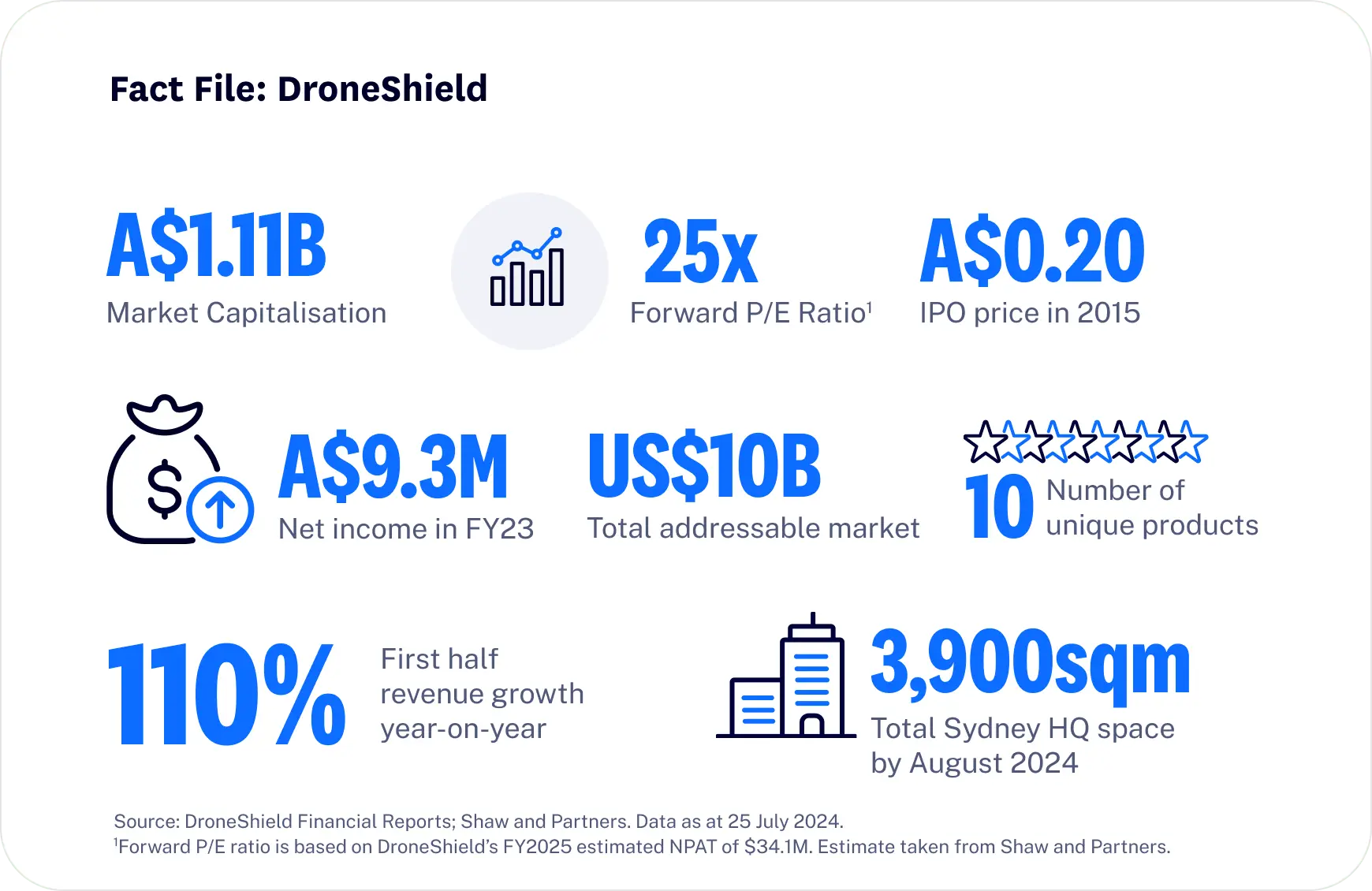

But perhaps that’s unsurprising – DroneShield’s share price hit a peak of 580% year-to-date before tumbling nearly 50% this July. This volatility took its market capitalisation of less than A$300m at the start of the year to over A$2 billion at its highest, and is currently at about A$1.1 billion.

So what exactly is DroneShield and what’s the story behind its volatility?

Let’s take a deep dive into Australia’s only anti-drone tech company.

What is DroneShield?

DroneShield is an Australian defence company that specialises in technology for drone detection and security. Its current product lineup includes handheld, vehicular and fixed hardware that can detect, analyse and shut down drones within a certain area. Its software can then compile this data, log it, integrate it into an existing API and analyse it using AI and machine learning technologies.

It’s one of the few companies in the world – and the only one in Australia – to already be supplying counter-drone hardware and software to customers globally. These include military and intelligence agencies (e.g. NATO), law enforcement, infrastructure and commercial entities.

This unique business profile and its high-profile customer base is why retail and institutional investors alike are keeping an eye on DroneShield.

“A $5,000 drone can blow up a $5 million tank… really highlights the need for counter-drone systems”

How DroneShield makes money

Now onto the exciting part… DroneShield’s financial statements.

There’s a lot to unpack, but to narrow it down to a few key points:

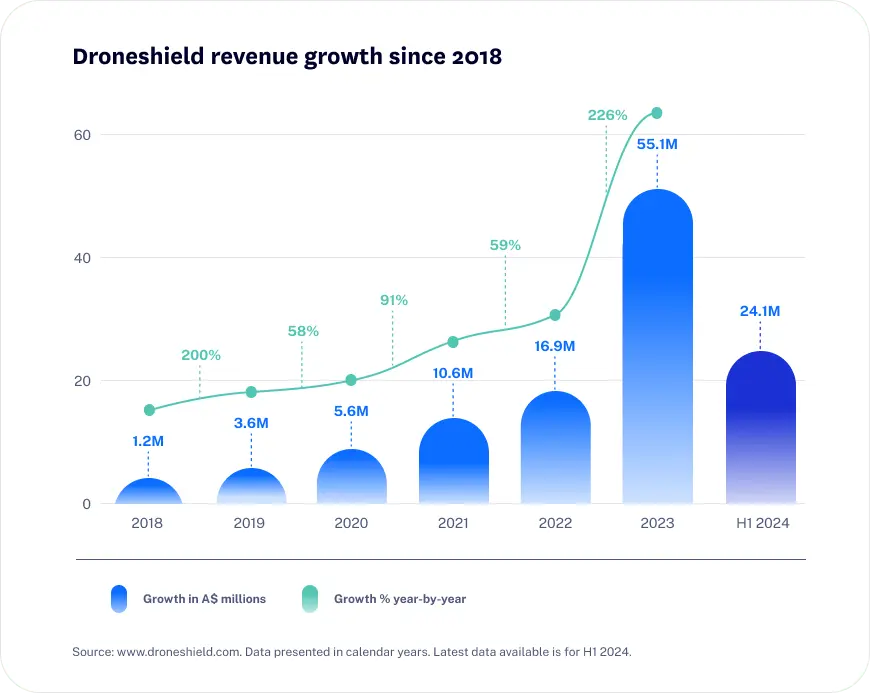

- Strong revenue momentum: DroneShield has recorded triple-digit revenue growth nearly every year since FY17.

- Growing sales pipeline: DroneShield has signed multiple customer contracts that add up to a total of $28m (as of 30 June 2024). It estimates a sales pipeline of more than $1.1 billion for 90+ projects.

- First year of profitability: DroneShield recorded its first year of profits in FY23 with a net income of $9.3m – up from a net loss of $949k the year prior.

- Recent equity raise to further boost cash: DroneShield completed an oversubscribed equity raise totalling $115m last quarter to boost R&D and inventory production.

- Zero debt: DroneShield boasts a balance sheet with zero short-term and long-term debt.

Revenue: Growth plus diversification

DroneShield has seen stunning sales growth in the last few years with total revenue jumping from $311k in FY17 to $55.1m in FY23.

Apart from rising geopolitical tension boosting government defence budgets, the use of drones in modern warfare has increased exponentially.

These two factors combined increased global demand for anti-drone tech – and DroneShield is the only publicly-listed company in the world with pure-play exposure to the industry.

Remember that past performance is not indicative of future performance. Graphics, charts and graphs provided for illustrative purposes only.

Apart from industry tailwinds, DroneShield’s product strategy also brought in favourable outcomes.

Just like how an iPhone works best with AirPods, DroneShield has also steadily developed its lineup of complementary tech. The use of DroneSentry-X Mk2 for example, is optimised by pairing with DroneShield’s DroneSentry-C2 software. Similar to Apple’s iOS updates, DroneShield constantly rolls out firmware updates such as its DroneLocator feature. But unlike the iOS, DroneShield capitalises on new tech by rolling out updates as part of a broader software subscription.

This subscription also allows DroneShield to diversify revenue drivers away from just hardware – allowing continuous revenue generation from customers who’ve already fully invested in DroneShield’s hardware.

Profitability: Low COGS plus zero debt

For a company that generates nearly 90% of its revenue from hardware sales, its overall gross profit margin of ~70% is noteworthy. Having COGS at less than a third of its total revenue allows DroneShield to invest in further R&D and marketing efforts. One of its most watched R&D initiatives at the moment is around the integration of AI and machine learning into its tech.

DroneShield has recently moved into its new 2,100 sqm headquarters. Additionally, DroneShield signed a lease for another 1,800sqm at its Sydney HQ, to bring its total space to 3,900sqm with a hardware production capacity of $500m. This paves the way for potential future revenue opportunities and increasing economies of scale.

Watch our recent tour of DroneShield’s shiny new HQ in Pyrmont, Sydney!

Additionally, DroneShield’s balance sheet is particularly impressive for a company that’s seemingly in the stage of high growth. DroneShield has kept its liabilities low by funding its expansion through equity raises instead of debt. The last time it recorded long-term debt in its statements was in FY 2020 – for a relatively miniscule amount of $43k.

While equity raising dilutes existing investor holdings, having zero debt means DroneShield isn’t subject to interest expense, which unlike marketing and R&D expenses, don’t necessarily bring value to DroneShield operationally. The lack of debt also lowers liquidity and solvency risks.

And now, the question is…

Can DroneShield continue growing?

In a recent interview, Oleg was quoted saying: “When we started eight years ago, there was no counter-drone industry. Drones were what you bought your child for Christmas. They were not a weapon.”

It’s hard not to agree – Drone technology is increasingly being used in armed conflict, with DroneShield estimating a total addressable market worth US$10 billion across military, law enforcement and infrastructure usage, among others.

While that sounds promising for DroneShield, the question is whether it can take advantage of it.

Bullish Outlook/Opportunities

- DroneShield has the potential to sign more supply contracts as governments increasingly invest in anti-drone technology amidst heightened geopolitical tensions.

- DroneShield may build a wider economic moat by strengthening its USPs and brand name, allowing it to be the global market leader in anti-drone technology.

- Drones could gain widespread usage both in and out of military applications, and DroneShield may capitalise on both. Some potential areas for growth outside of military applications include surveillance, security, law enforcement, surveying and mapping, delivery services, agriculture and construction.

- DroneShield could develop its software further and extend use cases to broader security systems.

Bearish Outlook/Risks

- DroneShield may be unable to capture new contracts and could exhaust its current pipeline.

- Demand for anti-drone technology may fall over time and DroneShield may not be able to adapt to the changing environment.

- Competitors could emerge and take market share, especially those domiciled closer to DroneShield’s existing customers. Note: About 70% of DroneShield’s FY23 revenues came from U.S.-based agencies.

- Lower cost anti-drone alternatives may emerge that threaten DroneShield’s competitive advantage.

- Legal and regulatory changes could potentially ban the use of drones or anti-drone tech, concurrently affecting the demand for DroneShield’s products.

Our CEO talks to Oleg about DroneShield’s future prospects in the video below.

Bonus Section: DroneShield: Founded in the U.S.

DroneShield was founded in 2014 in the U.S. by two former U.S. military men. The company was later sold to a private equity firm who wanted to list it in Australia, due to the ASX being “an enabler of small, innovative companies.” This is where DroneShield CEO, Oleg Vornik, made his entry into the company. A former investment banker with significant experience taking companies public, Oleg took DroneShield to the ASX in 2016.

While it still operates partially in the U.S., all its products are now developed and produced in Australia.

Did you know?

DroneShield was founded with the goal of using sophisticated acoustics to detect the “Mosquitoes”, before shooting it down with lasers. The idea didn’t really work out, so the founders instead used these acoustics to detect drones before shutting them down with jamming technology.

As always, it is essential to conduct your own research and due diligence before making any investment decisions. Superhero does not provide financial advice that considers your personal objectives, financial situation or particular needs. All investments carry risk so please consider carefully before investing. Remember that past performance is not indicative of future performance. Graphics, charts and graphs provided for illustrative purposes only.

Become a part of

our investor community

Why you should join us:

- Join free and invest with no monthly account fees.

- Fund your account in real time with PayID.

- Get investing with brokerage from $2. Other fees may apply for U.S. shares.

Read our latest articles

Make knowledge your superpower and up your skills and know-how with our news, educational tools and resources.